Somewhat aggressive accounting for its "U.S." and "Non-U.S. Pensions" and "Other Postretirement Benefit" plans ("pensions") understates the gravity of pensions in their reported earnings. However, Goodyear has been very forthright in discussing the cash flow implications of their underfunded pensions.

Contrary to Delta Airlines DAL and other firms we contacted, GT's IR department was quite willing to answer my questions about their pensions liabilities. More on DAL's looming pensions issues.

The company's stated plans to pay down its off-balance sheet liabilities depend on a fairly positive long-term economic outlook.

I think management at Goodyear is well-aware of their off-balance sheet issues and is taking steps to address them. However, if business headwinds persist, they simply may not have the cash flow required to overcome their pension liabilities.

If business does not remain buoyant, I think GT's earnings estimates will have to be lowered to reflect the looming pension liabilities.

Abnormal Pension Accounting Boosts EPS

GT boosted its 2011 earnings with a higher-than-average expected return on plan assets ("EROPA") assumption for its pensions of 7.70[1]%, down from 7.82% in 2010. Page 95 in GT's 2011 10-K filing has the details.

An EROPA of 7.70% is abnormally high. Out of the 1,021 companies with pensions that I cover, 63% of them have a lower EROPA. Only 96 of the 1,021 raised their EROPAs in 2012 while 525 lowered and 400 made no changes.

The 2012 EROPA looks a bit high compared to my estimates of the company's actual return on plan assets. I estimate 2011's actual return on plan assets was 3.19%. I estimate the average return over the last five years is 4.33%, over the past 10 years it is 6.40%, since 1998 it is 6.55%. These estimates are based on dividing the "Actual return on plan assets" by the "Beginning balance" of plan assets after adjustments suggested by GT's IR contact, Mike McCormick. You can replicate my analysis using data from the company's annual reports as detailed in the model used to calculate the actual return on plan assets, which is based on data from the 2011, 2010, 2009, 2008, 2007 and 2006-and prior 10-Ks.

Accounting Lowers Pension Expenses & Has Big Impact On EPS

Since GT's pensions are so large, its pension costs play a prominent role in earnings, much more so than most companies. GT's net periodic benefit cost after tax (the cost attributable to pensions with the current EROPA reported in GAAP earnings) is over 62% of 2011's net income.

Assuming a high EROPA enables GT to lower the costs it must report in earnings for paying into its pensions. In turn, the company's overall expenses are lower and accounting earnings are higher.

A 1% decrease in GT's EROPA would wipe away 7% of the company's 2011 net income, $35 million increase in pre-tax earnings, or $0.088 per basic shares outstanding. A 1% reduction to a 6.7% EROPA would be below the median (7.5%) EROPA for the 1,021 pensions we analyzed.

I think it is fair to say that GT is stretching the limits of its EROPA, which props up earnings.

Pensions Are Already Underfunded by $3.7 billion

One could argue that stretching the limits of EROPA and minimizing the amount of money it pays into its pensions is a fair and good strategy for a company whose pensions were adequately funded. That argument does not hold for GT as its pensions were under-funded by $3.7 billion as of 12/31/2011. The sum of the "net funded status" for the U.S., Non-U.S. and Other Postretirement Benefits" on page 93 of the company's 2011 10-K shows where I get the $3.7 billion value, which is about 1.5 times the company's market cap.

Doubtful That GT Can Grow Its Way Out Of Its Liabilities

If GT were in a high growth industry with excellent prospects for future profits, one could argue that the company could easily earn its way out of the underfunded pensions hole. That is a tough argument for a company in such a competitive and low margin business in a challenging economic environment.

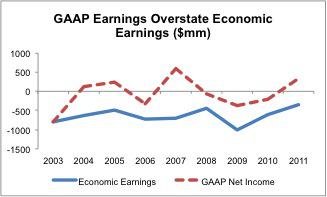

Despite reporting profitable GAAP accounting profits, my more comprehensive model suggests that GT is an unprofitable business even if one assumes its EROPA is fair and accurate. Figure 1 compares GT's economic earnings to its accounting earnings. In 2011, GT reported $321 million in accounting profit while I believe the company's true cash flows were closer to -$341 million.

Figure 1: Accounting Profits Are Rosy Too…Sustainable?

Sources: New Constructs, LLC and company filings

One of the largest drivers of the differences in reported accounting and economic earnings for GT is $1.1 billion in off-balance sheet debt from operating leases (about 45% of the company's market cap). In addition, Goodyear is in a very capital-intensive business and generates relatively little cash compared to the amount of invested capital in the business.

From where I sit, the company is in a tough situation. It is not making much, if any, money and its liabilities are formidable: pensions at $3.7 billion plus total debt of $6.3 billion equals $10 billion.

Equity Value Depressed By Growing Pension & Debt Liabilities

Last year, despite a significant increase in EPS compared to the prior year, the underfunded status of GT's pensions grew from $3.1 billion at the end of 2010 to $3.7 billion at the end of 2011.

Even if GT's liabilities do not increase, equity investors should be intimidated by the $10 billion in existing liabilities that have a senior claim on Goodyear's future profits. If Goodyear does generate future profits, those profits have to be large enough to cover the $10 billion in senior claims plus the expectations baked into the current stock price before equity investors can make significant money in GT.

$10 billion is more than 31 times GT's 2011 net income. Equity investors may be at the end of a very long line when it comes to expecting a payout from GT.

Stock Valuation Is Oblivious To Looming Liabilities

For those that say all of this information is already baked into the stock price, I suggest you look again. According to my discounted cash flow model, to justify the stock valuation at $10.83/share, the company has to grow its after-tax cash flow (NOPAT) by 4% compounded annually for 10 years. I underscore that those are the expectations baked into the current stock price. For investors to believe GT deserves a higher valuation/stock price, they must believe that the company's future profit growth will be even greater than that baked into the current stock price.

Footnotes Diligence Pays

In summary, using the footnotes to lift the accounting veil on GT's financial situation reveals some earnings and liabilities issues for a stock that is fairly expensive and could suffer downward pressure when investors concerned about these issues.

Avoid ETFs and Mutual Funds That Hold GT

Here is a list of the ETFs and mutual funds (as of June 12) that allocate the most to GT. Get free reports on these funds from my free mutual fund and ETF screener.

Mutual funds

- Investment Managers Series Trust: Towle Deep Value Fund (TDVFX) - Dangerous Rating

- Unified Series Trust: IMS Capital Value Fund (IMSCX) - Dangerous Rating

- LKCM Funds: LKCM Aquinas Value Fund (AQIEX) - Neutral Rating

ETFs

- Direxion All Cap Insider Sentiment Shares KNOW - Neutral Rating

- PowerShares S&P 500 High Beta Portfolio SPHB - Dangerous Rating

- Rydex S&P Equal Weight Consumer Discretionary RCD - Neutral Rating

Disclosure: I receive no compensation to write about any specific stock or theme.

[1] Value is the weighted average EROPA calculated using the average of the beginning and ending balance of the Fair Value of Plan Assets.

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.