The Past Week, In A Nutshell

What Happened: Stocks closed the week higher after investors regained optimism regarding a sustained recovery.

Remember This: “Earnings season has been very impressive so far, now you can couple that with the employment backdrop quickly improving as well. Not a bad combo for investors,” said Ryan Detrick, chief investment strategist at the LPL Financial.

“Still, let's be realistic, 10% unemployment isn't anything to get overly excited about and we still have a long way to go to get back to February levels of output.”

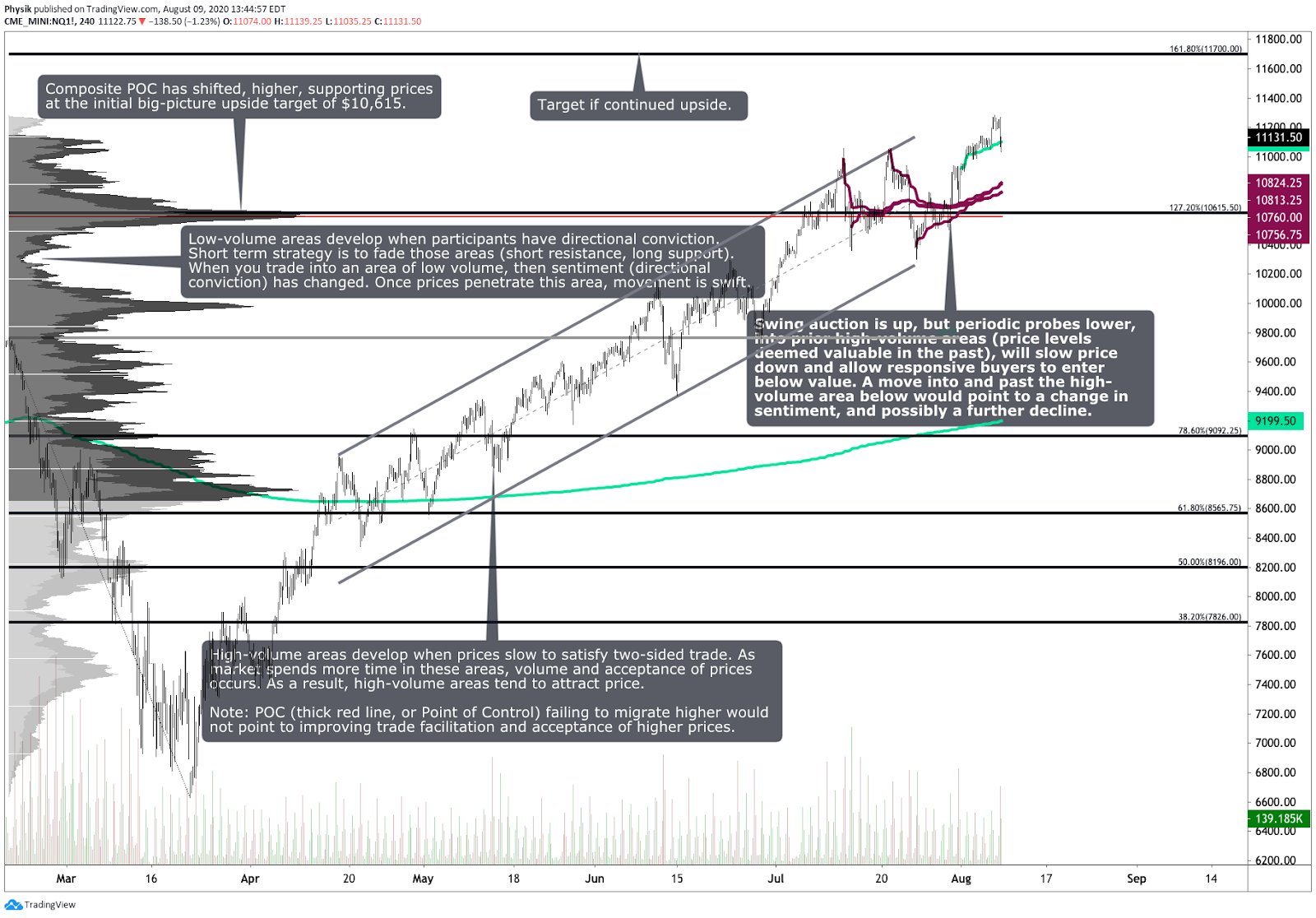

Pictured: Profile chart of the S&P 500 E-mini Futures

Technical: Broad-market equity indices resolved a prior balance area to the upside, evidenced by a successful breakout and migration of value.

Recapping last week’s action: On Monday, as M&A activity lifted sentiment and efforts to hammer out a coronavirus relief bill resumed, the S&P 500 moved out of a multi-week balance area, finishing further into the low-volume area left from the late February sell-off. Overnight, prices caught up to Monday’s divergent delta after disappointing earnings reports from Europe and a sharp rebuke from China. Tuesday’s U.S. session managed to get past the uninspiring news, closing higher and validating the breakout from balance.

Indices continued their trek higher Wednesday, closing and establishing value above prior balance on upbeat economic data and positive earnings. Pre-U.S. open, on Thursday, the S&P filled a prior gap, finding liquidity at the $3,300 strike before climbing higher, on poor structure and ahead of value, as investors reacted to upbeat jobless claims data.

Friday’s U.S. session further digested data on jobs, spending most of the cash session accepting value in the higher end of Thursday’s trading range, before squeezing into the close.

In light of mostly unchanged fundamental conditions, equity indices are positioned for further upside. Overall, the market appears to be migrating value higher, confirming the bullish trend. News regarding improving fundamentals and stimulus is likely to buoy the S&P in subsequent sessions. The potential exists, however, for a fast-moving correction of the poor structure left behind by the emotional, momentum-driven participants.

Scroll to bottom of this story to view non-profile charts.

Key Events: Earnings; JOLTS; NFIB Small Business Survey; Producer Prices; CPI; NAR Metro Prices; Import and Export Prices; Productivity; Industrial Production; University of Michigan Sentiment.

Fundamental: Best Buy Co Inc BBY announced its sales increased from last year.

- Software-as-a-Service and its potential impact on future business models.

- Fitch revises U.S. outlook, cites absence of a fiscal consolidation plan.

- Trump signed an order banning U.S. business with TikTok and WeChat.

- Twitter Inc TWTR, TikTok hold preliminary talks over combination.

- After a 2013 tax hike, the S&P posted its best annual gain in 16 years.

- Pfizer Inc PFE to make Gilead Sciences Inc GILD treatment.

- Eastman Kodak Company KODK to play a key role in generic drug making.

- Delta Air Lines Inc DAL wants 3,000 workers to take unpaid leave.

- Canada adds more jobs than expected in July; most were part-time positions.

- Trump signed an executive order restoring enhanced economic relief.

- Canada to impose retaliatory tariffs on U.S. goods, hopes for resolution.

- U.S. Postal Service chief warns of dire finances, adopts a hiring freeze.

- The U.S. earnings recovery may be faster than in previous crises.

- More businesses will tap the Fed’s loan program if the economy worsens.

- Federal Reserve, central banks are heading for a collision with shadow lenders.

- Understanding the disconnect between consumers and the stock market.

- Household debt, credit delinquencies dropped during Q2 recession.

- The U.S. shows signs of coronavirus peak, but difficult days lie ahead.

- Crude supplies are expected to remain ample for the foreseeable future.

- Auto sales turn a corner, carmakers post better than expected earnings.

- The U.S. and China have agreed to hold high-level trade talks on August 15.

- Apple Inc’s AAPL strong operating results reflect diversity, resilience.

- A 10% balance sheet expansion grows market returns by 7.4%, over 5-8 weeks.

- Europe’s global investment banks reduced operating leverage in Q2.

- Russia expands subsidized mortgage programs, supporting banks’ earnings.

- Why the Rocket Companies Inc RKT IPO is a paradigm shift in finance.

- LSE’s sale of MTS and Borsa Italiana stakes credit positive if proceeds reduce debt.

- Mexican insurers’ strong earnings enhance capacity to withstand economic contraction.

- The California Supreme Court upholds certain pension changes, maintains protections.

- U.S. will pay $1B for 100M doses of Johnson & Johnson’s JNJ vaccine.

- Canada signs deal with Pfizer Inc PFE, Moderna Inc MRNA.

- Record stimulus, liquidity surge to offset losses, open up the possibility of further upside.

- Hilton Hotels Corporation HLT sees demand rebounding to pre-virus levels.

- Bombardier Inc BDRBF sees higher deliveries of jet, misses quarterly profit.

- Governor Lael Brainard laid out the Federal Reserve’s instant payment framework.

- Negative real yields presage a weaker dollar, as well as higher gold prices.

- The job market recovery appears to be slowing as the services sector powers ahead.

- Berkshire Hathaway Inc (NYSE: BRK-A) bought Bank of America Corp BAC stock.

- Facebook Inc FB launches a TikTok-like product inside of Instagram.

- CVS Health Corp CVS in talks with the government over vaccines.

- Moderna Inc MRNA prices vaccines at $32-$37 per dose.

- Boeing Co BA does not see immediate need to raise cash with debt.

- Investors worried about the dollar’s status as the world’s reserve currency.

- Manufacturing activity jumped to its highest level in nearly a year and a half.

- Bank of America Corp BAC raised its gold target to $3,000/oz.

- Construction spending falls for the fourth straight month, but is still up from 2019.

- Twitter Inc TWTR may pay hundreds of millions in fines over a privacy issue.

- BP plc BP halves dividend after record loss, speeds up reinvention.

- Inflation in emerging markets is rising out of central bankers’ target ranges.

- Top CEOs urge Washington to get small businesses money as soon as possible.

- Economists at major investment banks worry about negative jobs growth.

- Fed policymakers call for fiscal support to save the U.S. economy.

- Canadian factory activity resumes expansion in July as the economy reopens.

- New orders for U.S.-made goods increased more than expected in June.

- New Ford Motor Company F CEO eyes expansion into technology.

- Air safety regulator gives no firm date for Boeing Co BA 737 MAX to fly.

- Advanced Micro Devices Inc’s AMD Q2 and outlook are credit positive.

- Deutsche Bank AG DB Q2 strengths in core business offset virus disruption.

- Credit Suisse Group AG CS Q2 capital markets businesses offset disruption.

- Microsoft Corporation MSFT to continue TikTok acquisition discussion.

- Marathon Petroleum Corp MPC agreed to sell gas stations to 7-Eleven.

- Chipotle Mexican Grill Inc CMG, fast food brands set for new hiring wave.

- Alphabet Inc Class A GOOGL unveils 5G phones, cuts Pixel price.

- Alphabet Inc Class A GOOGL to buy a stake in ADT home security.

- Sentiment: 23.3% Bullish, 29.1% Neutral, 47.6% Bearish as of 8/5/2020.

Product Snapshot

S&P 500 E-mini Futures (ES) | SPDR S&P 500 ETF Trust SPY

Nasdaq-100 E-mini Futures (NQ) | PowerShares QQQ Trust QQQ

Russell 2000 E-mini Futures (RTY) | iShares Russell 2000 Index IWM

Gold Futures (GC) | SPDR Gold Trust GLD

Crude Oil (CL) | United States Oil Fund LP USO | Invesco DB Oil Fund DBO | United States 12 Month Oil Fund USL

Treasury Bonds (ZB) | iShares 20+ Year Treasury Bond TLT

Cover photo by Nicolas Donati from Pexels.

Edge Rankings

Price Trend

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.