We are 9 days away from the debt ceiling deadline. As of right now there’s no deal. Here are the effects of a breach according to Moody’s:

1 week: 1.5 million jobs lost, raising the unemployment rate from 3.4% to 5%.

2 months: 8 million jobs lost, raising the unemployment rate from 3.4% to 7.8%.

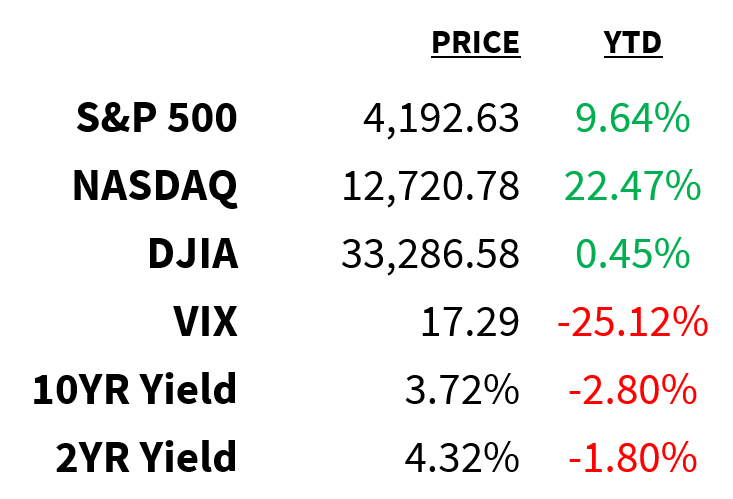

Market

Prices as of 4 pm EST, 5/22/23

Macro

President Biden and House Speaker McCarthy met again last night to continue debt ceiling discussions.

-

No deal was struck but both admitted the evening’s talks were productive, with the Speaker calling them “better than any other” thus far.

-

The meeting followed another letter from Janet Yellen who once again warned the Treasury was “highly likely” to run out of cash by early June.

-

Meanwhile, Treasury markets are discounting at least some chance of a default: yields on 1-, 2-, 3-, 4-, and 5-month T-bills are now all higher than the Fed funds rate.

Four Fed presidents spoke yesterday—here’s what they said:

-

St. Louis’ James Bullard was the most hawkish, backing 2 more rate hikes this year to fight inflation.

-

San Francisco’s Mary Daly expressed the need for caution, declining to commit one way or another.

-

Atlanta’s Raphael Bostic advocated for a pause amid emerging tightness.

-

Richmond’s Thomas Barkin remains unconvinced inflation has been defeated and declined to “prejudge” the June decision.

-

Market probabilities for a pause next month are currently hovering around 80%.

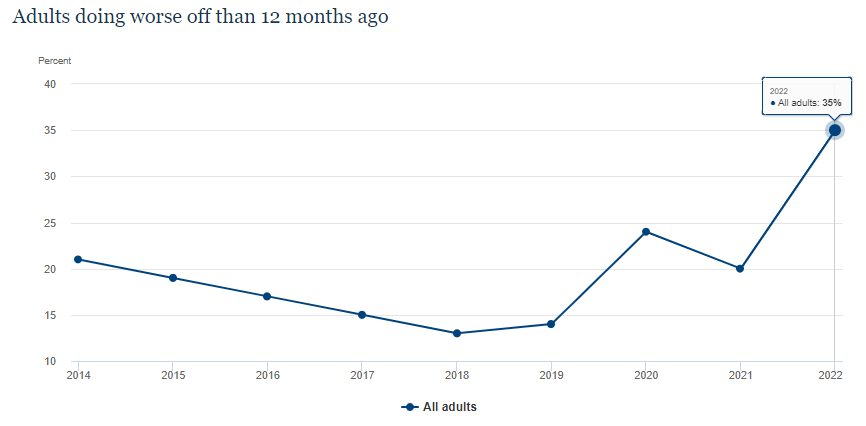

According to a Fed household survey, Americans’ financial well-being is declining.

-

73% of adults reported “at least doing okay financially”, down from 78% in 2021 and the lowest since 2016.

-

Shares of respondents who could cover unexpected emergency expenses, had 3 months of emergency savings, and were able to pay their current bills in full all dropped.

-

The percentage who reported being worse off financially than a year earlier jumped from 20% to 35%, the highest since the question was first asked in 2014 (by far).

Stocks

America’s biggest bank, JPMorgan, held its investor day yesterday–here are some highlights:

-

CEO Jamie Dimon did his best Jordan Belfort impression, declining to offer a timeline about when he might be stepping down.

-

Expecting a boost from its First Republic acquisition, the bank raised its net interest income forecast to $84 billion from $81 billion.

-

Investment banking and trading, on the other hand, is expected to decline 15% YoY.

-

Dimon warned commercial real estate loans were likely to create problems for some banks.

Speaking of, regional bank stocks followed through on last week’s gains on Monday.

-

Performance was led by shares of PacWest (+19%) after it announced the sale of a $2.6 billion loan portfolio.

-

The deal is part of the bank’s strategy to pursue strategic asset sales.

-

Other bank stocks enjoying outsized gains include First Foundation (+12%), Western Alliance (+10%), and Customers Bancorp (+10%).

After 5 straight weeks of selling, hedge funds rushed into US stocks over the past 14 days.

-

The pace of buying was the fastest since October.

-

Nobody wants to tell their boss they were sitting on the sidelines - is FOMO kicking in?

-

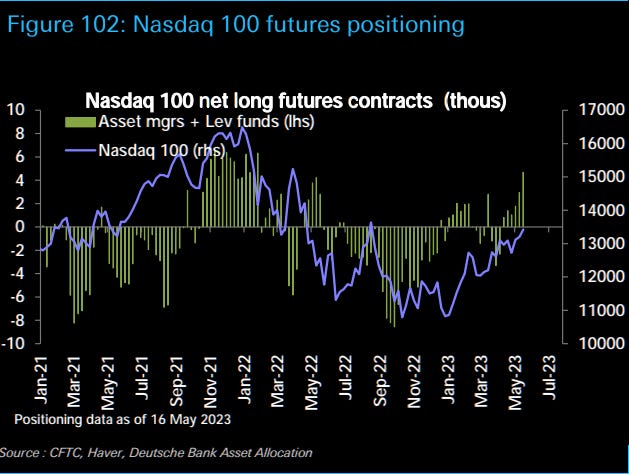

In terms of positioning, short positions in S&P futures are at their most bearish since 2007.

-

On the other hand, asset managers are most long Big Tech since early 2022.

-

According to Bloomberg’s Simon White, hedge funds are likely net long equities.

Energy

Saudi Energy Minister Prince Abdulaziz issued a warning to short-sellers:

-

“I keep advising them that they will be ouching”

-

OPEC+ is set to meet on June 3-4 to discuss production policy for the second half of 2023.

-

Will the alliance make another surprise cut to production similar to April’s move?

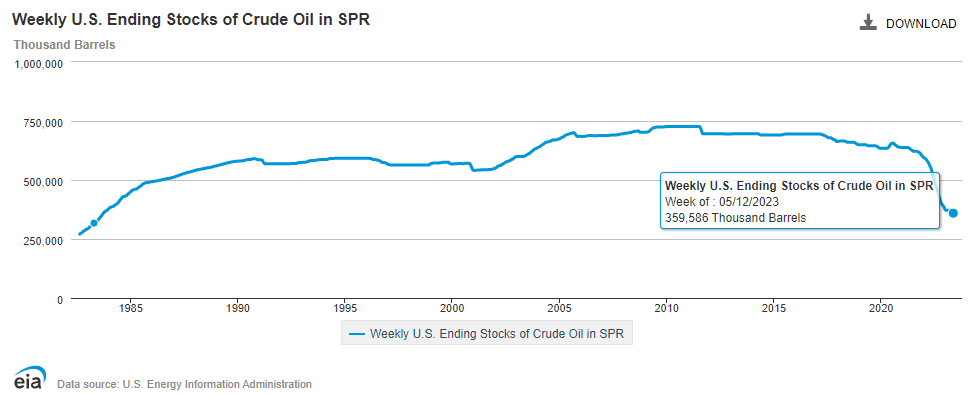

Last year, the White House sold more than 180 million barrels from the US Strategic Petroleum Reserve (SPR).

-

While releases continue, it has expressed its intent to replenish reserves by 60 million barrels.

-

Doing so, however, will be a challenge: early attempts to buy crude with fixed-price proposals didn’t take and now the Energy Department is attempting to think like an oil trader.

-

Its next attempt will employ different pricing approaches with proposals due May 31.

Earnings

Yesterday’s highlights:

Zoom ZM: $1.16 EPS (vs. $0.99 expected), $1.1 billion in sales (vs. $1.08B expected).

-

Its enterprise customer base increased 9% YoY while those generating more than $100,000 jumped 23%.

-

Current quarter guidance was in line with consensus forecasts.

-

The company also lifted its outlook for revenue and earnings for FY2024 above Wall Street’s estimates.

What we’re watching today:

-

Intuit INTU

-

Lowe’s LOW

-

Palo Alto Networks PANW

-

Autozone AZO

-

Agilent Technologies A

-

Dick’s Sporting Goods DKS

-

BJ’s Wholesale Club BJ

-

Vipshop VIPS

-

Williams-Sonoma WSM

-

V.F. VFC

-

Toll Brothers TOL

-

New Relic NEWR

Top Headlines

-

Default worries: Investors are shifting from US Treasury bills to bonds issued by top-rated American companies.

-

S&P FOMO: Investors added $21 billion in new long positions to S&P 500 futures, outnumbering shorts by more than 9-to-1.

-

Bond rush: After last year’s $332 billion of outflows, more than $100 billion has poured into fixed income funds during the first 4 months of 2023.

-

Carbon credits: JPMorgan will invest over $200 million to purchase credits from carbon removal startups.

-

Full access: TikTok will grant Oracle full access to its source code, algorithm, and content-moderation material.

-

Responsible AI: In an article written for the Financial Times, Google CEO Sundar Pichai emphasized the importance of building AI responsibly.

-

Reputation rankings: The most visible brands in America, according to 20 years of Harris Poll research.

-

UK is OK: The IMF predicts that the UK will avoid a recession this year thanks to resilient demand and declining energy prices.

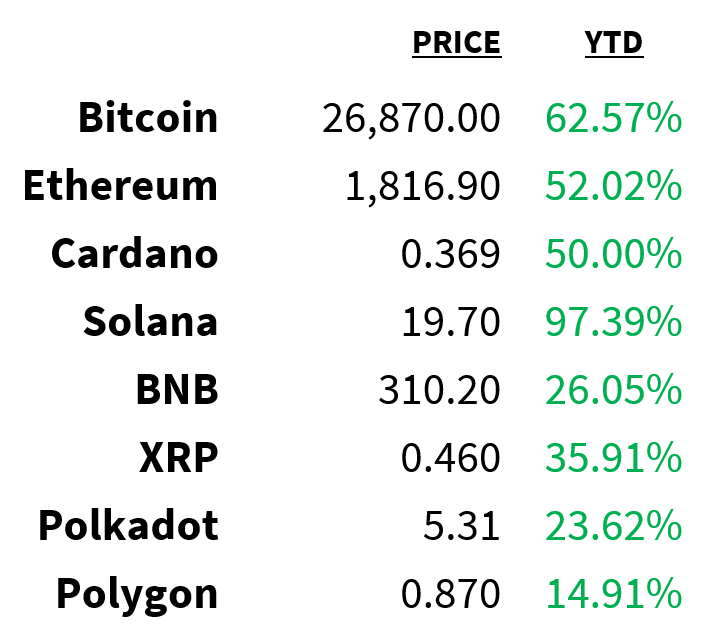

Crypto

Prices as of 4 pm EST, 5/22/23

-

Asset flows: Digital asset investment products saw their 5th straight week of outflows totaling $32 million.

-

Staked ETH: The number of ether staked in the Ethereum network has reached a record high of 22.58 million.

-

Russian sanctions: The Russian Foreign Ministry has banned several high-profile industry names from crypto firms, think tanks, and government agencies.

-

Taming crypto: The global securities watchdog, Iosco, is urging regulators to act more quickly and boldly on crypto markets.

-

Exchanges welcome: Hong Kong’s Securities and Futures Commission (SFC) will start accepting license applications for crypto exchanges on June 1.

Deals

-

Shale double down: Chevron has acquired O&G rival PDC Energy for $6.3 billion in an all-stock deal.

-

Terminated: TV operator Tegna has ended its $8.6 billion merger agreement with hedge fund Standard General.

-

AI funding: AI startup Builder.ai has raised $250 million in a round led by the Qatar Investment Authority.

-

Recommendations: Activist investor TCS Capital Management has acquired a +4% stake in Yelp and is pushing for a sale.

-

Streaming merger: Paramount+ and Showtime will combine forces starting June 27 (at higher prices).

-

Meme Of The Day

Edge Rankings

Price Trend

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.