In last week’s note, Labor Market Conundrums, we discussed questions raised by the last couple of employment reports about labor market demand, supply and where the two shall meet, wage growth. One report does not make a trend, however, the combination of trends that were in place for most of ‘23, combined with the January Job Openings and Labor Turnover Survey, the February Conference Board Labor Differential, the NFIB Small Business Survey and the February Employment Report, all significantly increased our confidence in our quadrilemma thesis. As our Bloomberg ECO screen populated at 8:30 eastern, the uptick in the unemployment to 3.9%, attributable to a third consecutive decline in household survey employment and a rebound in the labor force due in part to the prime age participation rate rising to 83.5%, the best level since 2002, and a 0.1% increase in average hourly earnings, put us back on track for a 4+% unemployment rate and wage growth below 4%, which triggers a Fed cutting cycle to 4% and keeps the 10-year note in the vicinity of 4%.

One month is not sufficient to change the Fed’s ‘confidence narrative’, however, the February report will nudge them back towards the supply-side recovery wage disinflation outlook particularly if we get cooler readings on CPI non-housing services inflation on Tuesday. From our perspective, there was another decline in labor market reallocation to the lowest level since August 2014 when the Fed was Re-Evaluating Labor Market Dynamics in Jackson Hole and Davis and Haltiwanger’s paper, Labor Market Fluidity and Economic Performance, that introduced the worker reallocation model, kicked off the proceedings. Our work concludes that at least half of the wage level shock was attributable to the Great Reallocation from mid-’21 to mid’-’22, the greatest level of churn in the labor market since the data became available in 2001. The persistent decline in reallocation, as evidenced by the Quits Rate plunging from 3% to 2.1%, which is back to 2017 levels, projects wage growth below 3% in a year’s time. Getting back on track with a cutting cycle to 4% in reasonably short order is crucial to loosening the bank credit channel.

We will dig into the details of last week’s labor market reports, summarize how our trip to NYC informed our outlook, discuss the outlook for the administration’s bank capital proposal following Chairman Powell’s Monetary Policy report to Congress, provide thoughts on divergent financial conditions, and update our sector and asset allocation outlook in this week’s note.

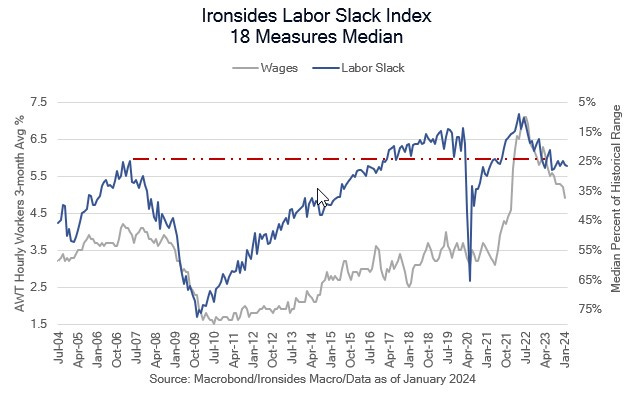

Figure 1: Our broad measure of labor slack stalled at mid-year ‘23, however wage growth cooled throughout the period with the exception of a couple of months in the least robust series, average hourly earnings. A 0.1% monthly increase in that series put our reallocation wage model back on track.

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.