(Photo - Jim Allen/FreightWaves)

Recent releases by Ryder System R and Knight-Swift KNX highlight the growing awareness of the added costs required for fleets that face increased pressure to transition to electric vehicles. A major challenge for long-haul trucking is cost, and current incentives from the Inflation Reduction Act only cover up to a maximum of $40,000 for commercial clean vehicles weighing over 14,000 pounds. A new Class 8 battery electric vehicle is significantly more expensive.

For Knight-Swift, the added cost puts the vehicles beyond profitability. The company said in a recent SEC filing, "There currently is an approximately $200,000-$300,000 new equipment cost differential between an internal combustion engine Class 8 tractor (a tractor weighing over 33,000 lbs., which comprise the majority of our fleet), and an EV alternative. Apply this cost over our fleet of approximately 27,500 tractors and the cost is beyond our ability to fund in an efficient manner." Knight-Swift highlighted the lack of range, noting, "Additionally, our two years of piloting the EVs currently available to our industry have shown a disappointing mileage range of approximately 165 miles compared with the Company's average length of haul of just under 500 miles."

The problem is not isolated to fleets but also to those who lease to them. Ryder System recently released an analysis that compared the total cost to transport (TCT) goods by diesel with that of battery electric vehicles. The results showed significant increases in total costs for heavy-duty EV tractors.

"And, for a heavy-duty EV tractor (Class 8), the annual TCT increases by approximately 94% or approximately $315,000" the report states. "The equipment cost is the largest contributor, representing an increase of approximately 500%, followed by general and administrative costs that increase approximately 87%, and labor and other personnel costs that increase 76% and 74%, respectively. Fuel versus energy savings are approximately 52%."

April CMV forecasts, trailer demand forecast revision, used Class 8 auction prices

ACT Research recently updated its commercial motor vehicle forecast, which saw significant revisions to trailers. The release notes that persistent Class 8 overcapacity continues to weigh down carrier profitability. Kenny Vieth, ACT's president and senior analyst, said in the release, "We revisited our trailer forecasts based on these near-term considerations: carrier profits, overstocked trailer dealer inventories that are proving hard to move, a short and soft peak order season, and increasingly diminished backlogs."

Less profits also mean sacrifices when upgrading aging tractors and trailers. During lean times, fleets upgrade tractors first, as newer units lower the overall maintenance cost per mile. Vieth notes, "There is a historically strong relationship between carrier profits and vehicle demand. Once a quarter, we get to look at the publicly traded truckload carriers' financial performance. The opening stanza of 2024 was notably bad for the very good carriers who make up the group. In Q1, profit margins collapsed to a 14-year low 2.6% (3.0% seasonally adjusted)."

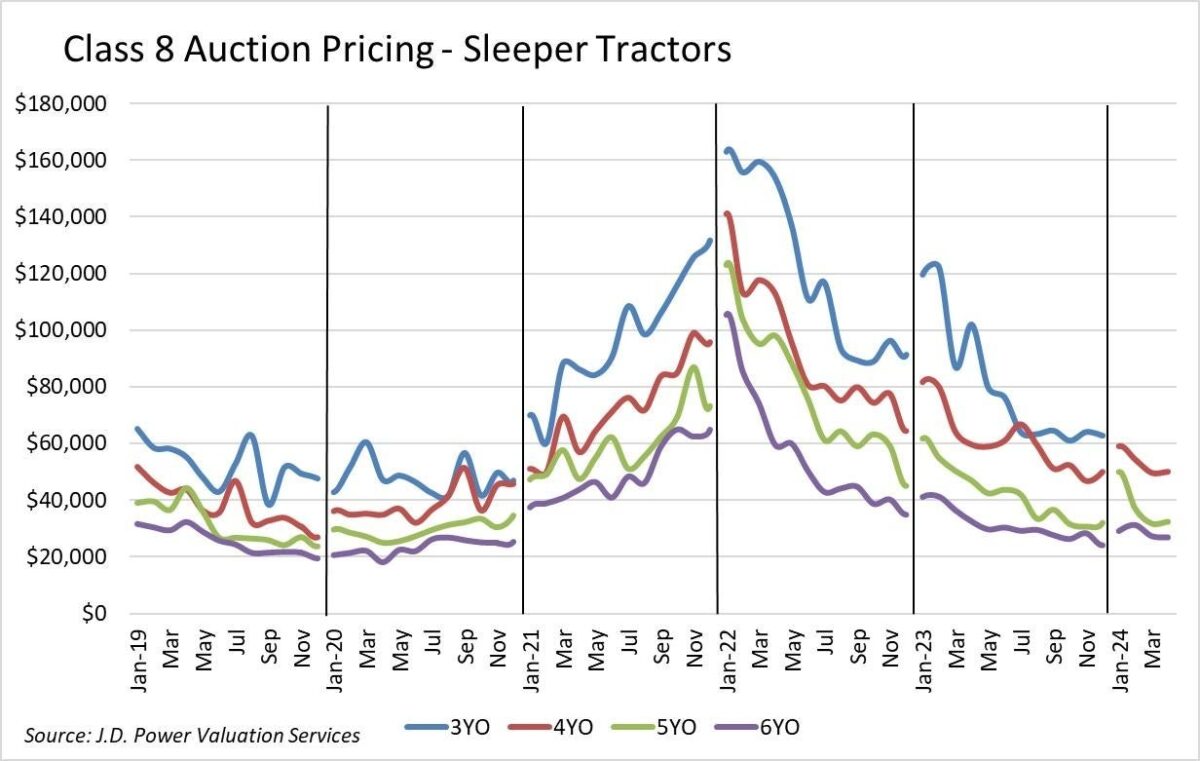

For fleets that cannot afford newer Class 8 units, recent auction data from J.D. Power suggests that used tractors are looking more attractive. Regarding pricing trends, a J.D. Power report states that for late-model sleeper tractors, the average April price for its benchmark truck was:

- Model year 2021: $50,173, $357 (0.7%) higher than March.

- Model year 2020: $32,433, $640 (2%) higher than March.

- Model year 2019: $26,749, $457 (1.7%) lower than March.

- Model year 2018: $19,301, $2,197 (10.2%) lower than March.

Despite the ongoing declines in auction prices, fleets looking for used equipment should pay attention to the mileage. The report adds, "However, anyone watching the large number of trucks with very high mileage for their age run through the lanes would be excused for feeling like trucks were bringing less money."

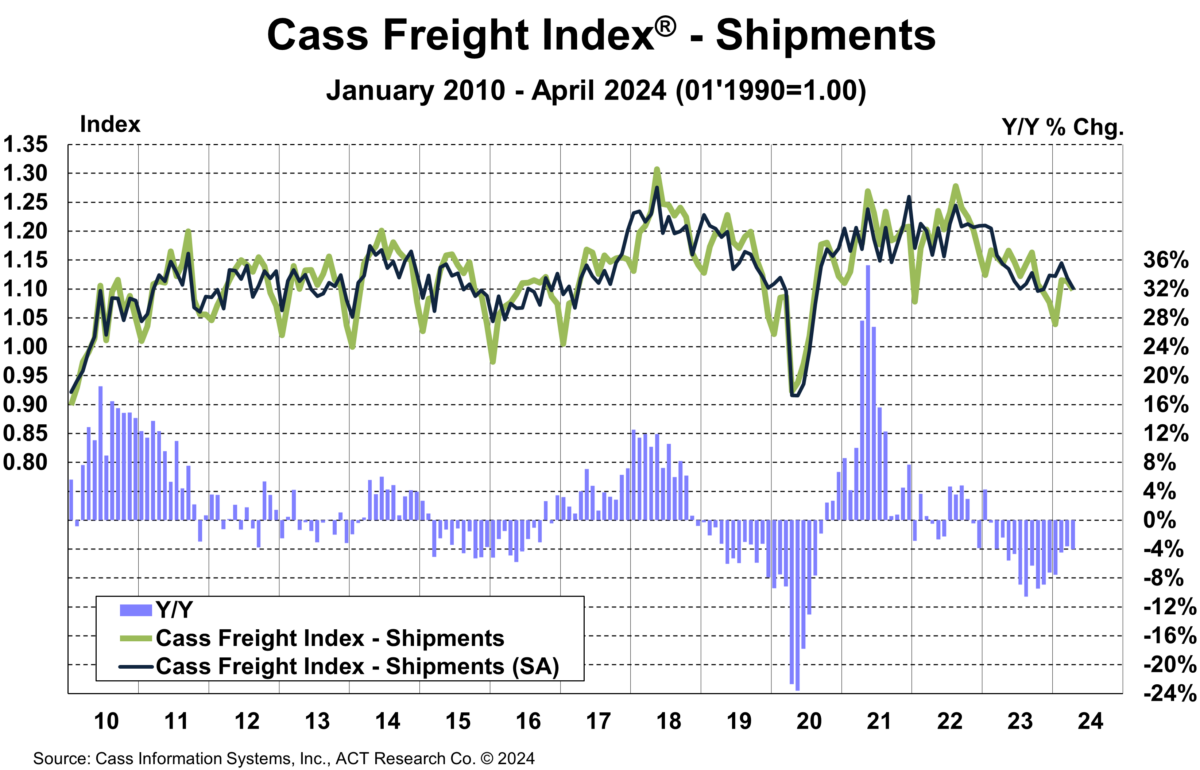

Market update: Cass April data mostly stable; private fleets poach spot market freight

On Tuesday, freight audit and payments provider Cass Information Systems released its April Transportation Index data, which saw a freight market relatively little changed from March. The shipments component of the Cass Freight Index fell 1.3% compared to March, 1.6% seasonally adjusted as the for-hire segment remains soft. The report notes that while Lunar New Year and the Baltimore bridge collapse may have temporarily impacted the April data, there is a potential risk for further shipment volume declines moving into Q2.

The past few Cass Index reports noted the impact of private fleet growth and how it leaches capacity from for-hire carriers. This trend continues and may have accelerated in April. The report notes, "For-hire fleets likely still are seeing soft demand because of significant private fleet capacity additions in the past couple of years. Private fleets are now more actively competing for spot freight to fill empty backhauls, lengthening below-trend for-hire demand levels."

For carriers in the for-hire space, the long-term competition remains railroads, not private fleets. Private fleets will search for backhauls if their internal demand permits it, but this is a temporary approach until their internal truckload demand improves. The downside is private fleet activity on the spot market will continue to depress spot rates. The report concludes, "To the extent private fleets are successful filling backhauls, it will further delay the for-hire cycle. The good news is that they're not nearly as cost-effective as for-hire fleets, so it will turn eventually."

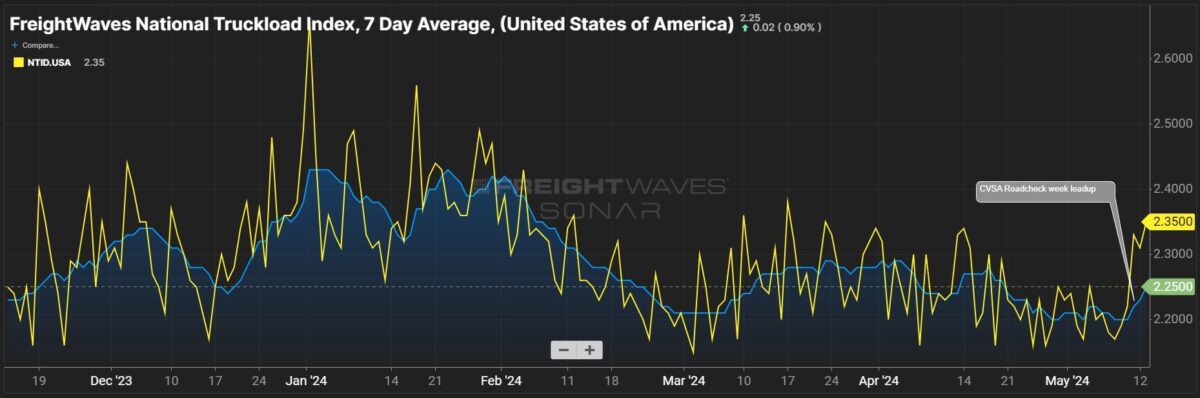

FreightWaves SONAR spotlight: Roadcheck event pulls spot rates higher

(Source - FreightWaves SONAR)

Summary: Daily spot market rates surged during the annual Commercial Vehicle Safety Alliance International Roadcheck, which began Tuesday and runs through Thursday. The FreightWaves National Truckload Index Daily jumped 15 cents per mile over the weekend from $2.20 all-in on Friday to $2.35 per mile, the highest daily figure since April 14. The large jump pulled up the NTI seven-day moving average to $2.25 per mile, an improvement of 4 cents week over week from $2.21 on May 6.

Dry van spot rates were not the only segment to see gains. Reefer spot market rates jumped 6 cents per mile all-in from $2.45 on May 9 to $2.51. For reefer carriers exposed to contracted freight, produce season paired with Roadcheck also saw outbound tender rejection rates increase. Reefer outbound tender rejection rates rose 109 basis points w/w from 3.93% on May 6 to 5.02%.

Looking ahead, questions remain about whether spot market rate gains will continue following Roadcheck, or if excess trucking capacity will continue to weigh down spot market rates for both dry van and reefer carriers. Small fleets and owner-operators remain resilient despite higher costs paired with lower freight rates. Net declines in operating authorities have begun to moderate in Q1, with March seeing three weeks of recorded overall gains in trucking authorities on weeks ending March 1, 15 and 22, according to data from Carrier Details Net Changes in Trucking Authorities. Carrier exits resumed in April and May but at lower rates, suggesting that despite ongoing carrier exits, new players continue to enter the marketplace. One theory is that lower used truck prices are an attractive proposition for carriers attempting to jump into the marketplace before spot rates increase.

The post Trucking electrification throttled by excessive ownership costs appeared first on FreightWaves.

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.