Index futures are gaining momentum on Tuesday, signaling an acceleration upward as the “Santa Claus” rally takes hold. Adding to the positive sentiment is an early Christmas gift from the Bank of Japan, which has maintained its ultra-loose monetary policy. Traders will also be navigating through earnings reports and housing starts data as potential catalysts.

Bond yields remain subdued, and crude oil continues its fluctuating trajectory.

Highlights from Monday's Trading:

- U.S. stocks maintained mostly positive momentum, with the Nasdaq Composite and the S&P 500 Index finishing notably higher. The S&P 500 closed at its highest level since Jan. 4, 2022, and the Nasdaq Composite reached its highest point since Jan. 12, 2022.

- The Dow Industrials closed flat but with a slight upward bias, achieving another record closing high. Small-cap stocks experienced some volatility during the session.

- Investors, anticipating rate cuts in the new year, have seen a resurgence in risk appetite, driving increased buying interest.

- Within S&P sector classes, communication services and consumer staple stocks showed significant gains, while most others traded with muted activity.

US Index Performance On Monday

| Index | Performance (+/-) | Value |

| Nasdaq Composite | +0.62% | 14,904.81 |

| S&P 500 Index | +0.45% | 4,740.56 |

| Dow Industrials | +0.00% | 37,306.02 |

| Russell 2000 | -0.14% | 1,982.42 |

Analyst Color:

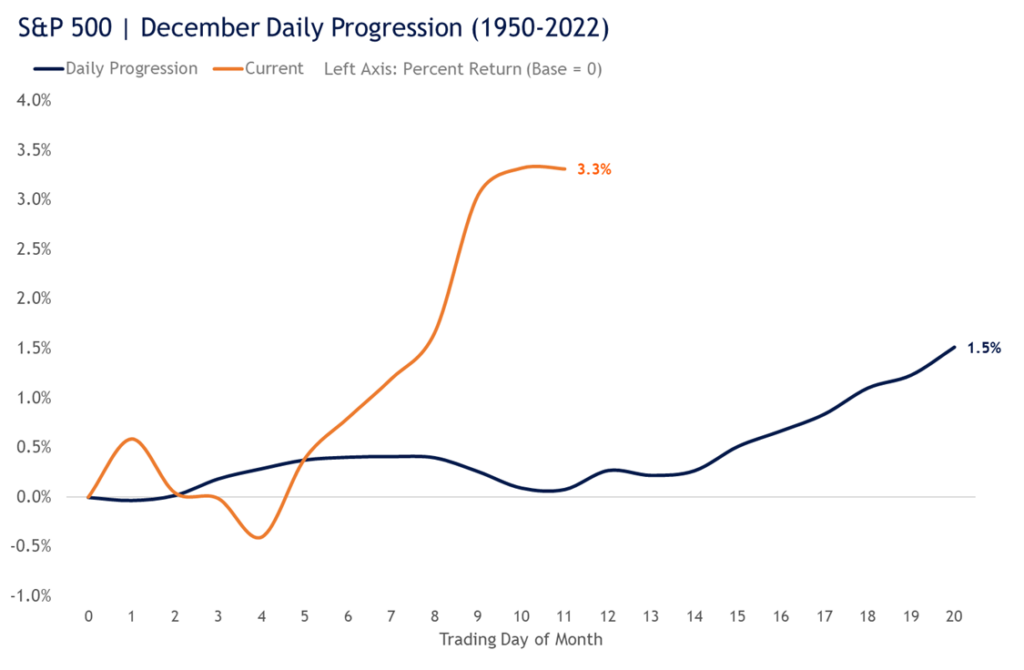

December is typically a “second-half story,” said LPL Chief Technical Strategist Adam Turnquist. Since 1950, the S&P 500 has generated an average gain of 1.5% in December and finished higher 74% of the time, he said.

“Most of the gains during the month have come during the second half, as the average gain at the halfway point is only around 0.1%,” Turnquist said. This year, the index was clearly outpacing its average December progression, he noted.

“Of the six prior years when the S&P 500 had a mid-month gain of at least 3%, the index added another 1.5% in the second half of the month to finish December with an average of 5.8%,” he said.

Chart Courtesy of LPL Financial

Futures Today

Futures Performance On Tuesday

| Futures | Performance (+/-) |

| Nasdaq 100 | +0.11% |

| S&P 500 | +0.11% |

| Dow | +0.09% |

| R2K | +0.44% |

In premarket trading on Tuesday, the SPDR S&P 500 ETF Trust SPY rose 0.12% to $472.55 and the Invesco QQQ ETF QQQ gained 0.13% to $407.62, according to Benzinga Pro data.

Upcoming Economic Data:

The Commerce Department is due to release the housing starts and building report for November at 8:30 am ET. Economists, on average, expect housing starts to come in at a seasonally adjusted annual rate of 1.360 million units, down from 1.372 million units in October. Building permits, a leading indicator of housing starts, may have slipped from 1.498 million units to 1.470 million units.

Richmond Fed President Thomas Barkin is due to speak at 9:30 a.m. ET and Atlanta Fed President Raphael Bostic at 12:30 pm ET.

See also: Futures Vs. Options

Stocks In Focus:

- Plug Power, Inc. PLUG fell nearly 4% in premarket trading following a negative analyst action.

- Accenture plc ACN, FactSet Research Systems Inc. FDS, and FuelCell Energy, Inc. FCEL are among the companies due to release their quarterly results ahead of the market open.

- FedEx Corporation FDX, Steelcase Inc. SCS, and Worthington Enterprises, Inc. WOR will report after the market close.

Commodities, Bonds, Other Global Equity Markets:

Crude oil futures fell 0.16% to $72.70 in early European session on Tuesday, reversing some of the 1.95% gain they notched up on Monday.

The benchmark 10-year Treasury note fell 0.043 percentage points to 3.913% on Thursday.

Most major markets in Asia advanced on Tuesday, led by the Japanese, Australian and Indonesian markets. Traders welcomed a central bank decision from the region as the Bank of Japan’s Monetary Policy Board announced its verdict to keep its ultra-loose monetary policy intact.

European stocks posted gains in late-morning trading, although trading was marked by listlessness. The EURO STOXX 50 Index, a stock index of Eurozone stocks, rose modestly.

Image created with artificial intelligence on MidJourney

Edge Rankings

Price Trend

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.